From Foundations to Fault Lines — Part I

In this series: Part I: Cracks in the Foundations Part II: Collateral Fragility Part III: Seemingly Stable, Systemically Stressed

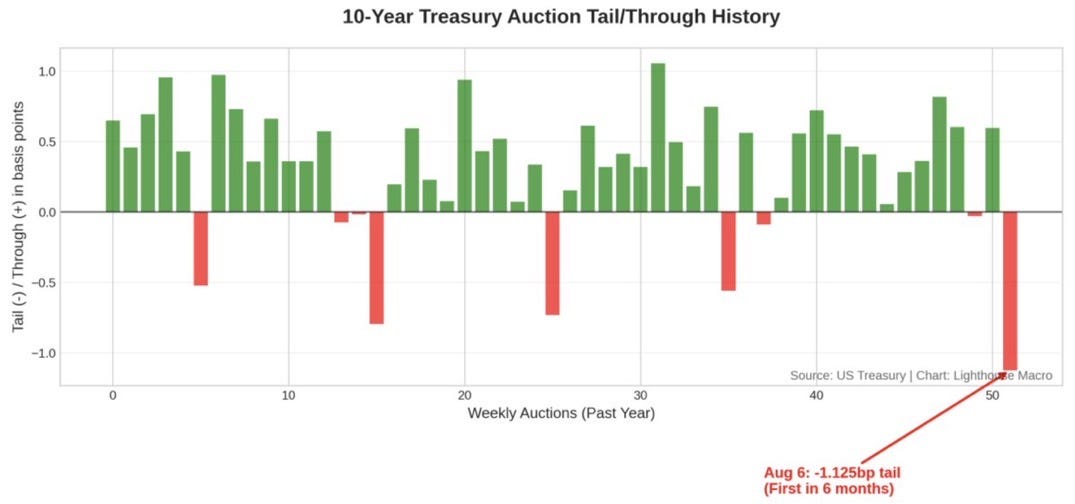

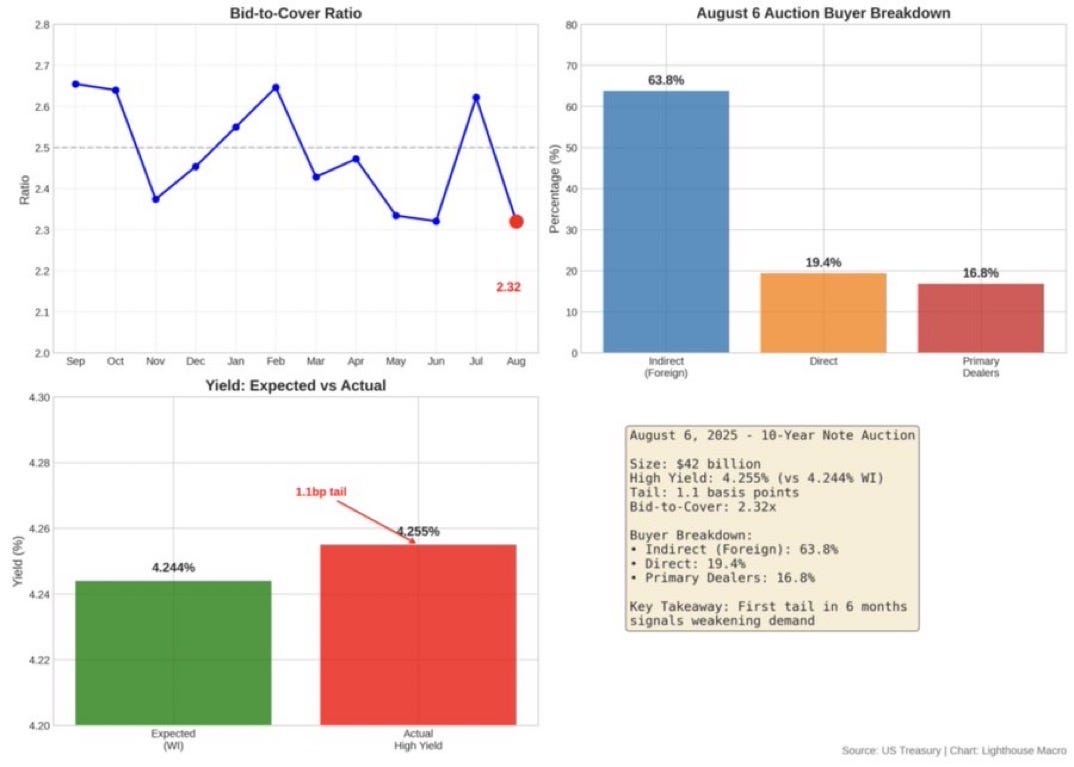

The foundation of demand for U.S. Treasuries, particularly at the long end of the curve, is showing signs of structural weakness. Yesterday's 10-year auction tailed 1.125 basis points—meaning it sold at a higher yield than expected—the first tail in six months, forcing the government to pay 4.255% instead of the expected 4.244% to clear $42 billion in debt. This isn't just one bad auction; it's a symptom of a deeper shift in market dynamics that investors can no longer ignore.

The Changing Face of Treasury Demand

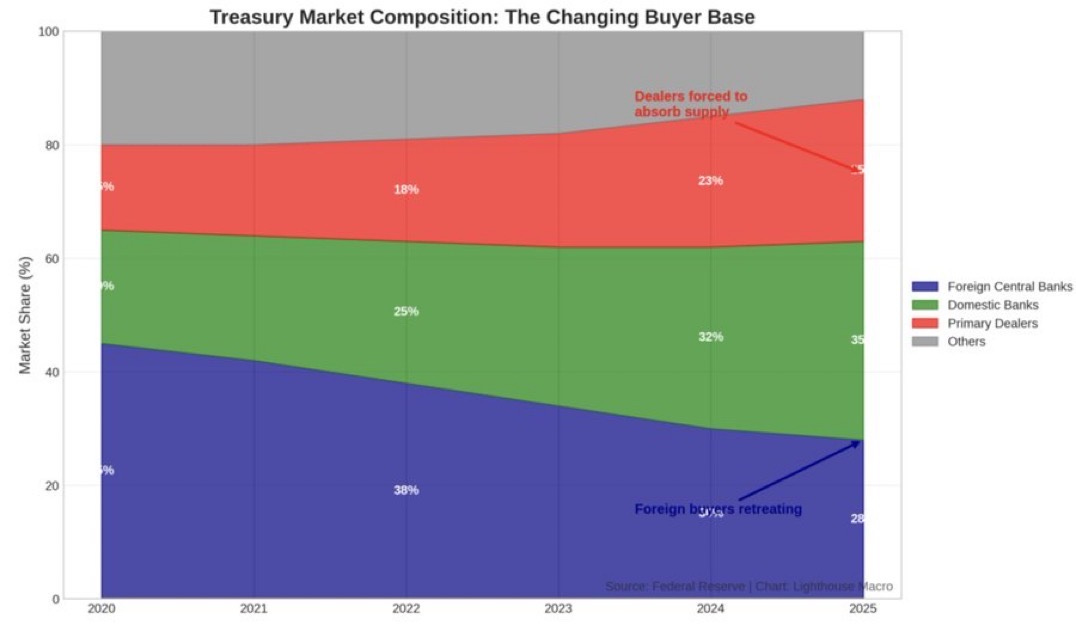

The composition of Treasury buyers has undergone a dramatic transformation. Foreign central banks, once the reliable backbone of demand, have seen their market share decline from 45% in 2020 to just 28% today. This retreat has forced domestic banks and primary dealers to fill the gap, with banks increasing their holdings from 20% to 35% and dealers rising from 15% to 25%.

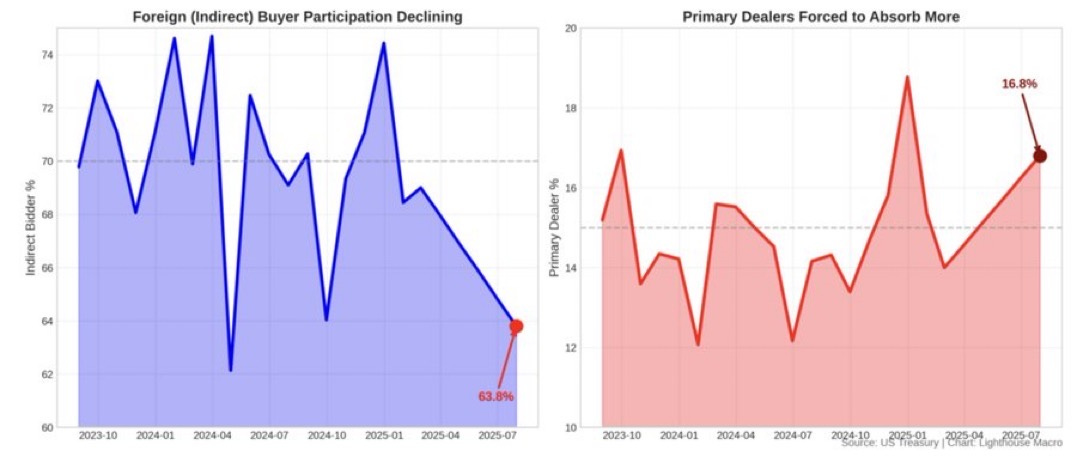

These aren't natural buyers—they're intermediaries being forced to warehouse risk they don't want. The August 6 auction results tell the story: bid-to-cover ratios at 2.32x, foreign demand at 63.8% (down from historical averages near 70%), and dealers forced to absorb 16.8% of the issuance.

Dealer Constraints Approaching Breaking Point

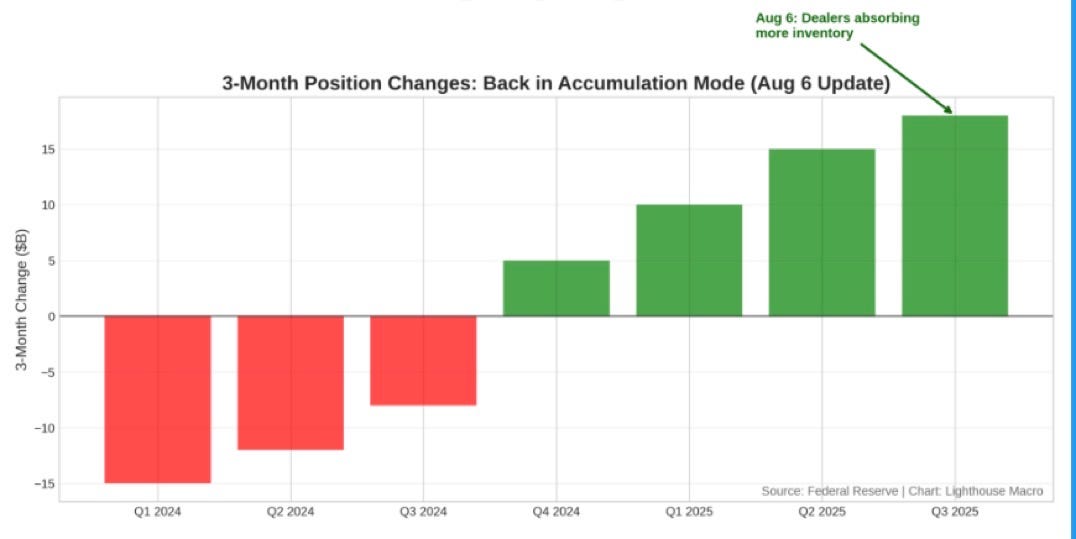

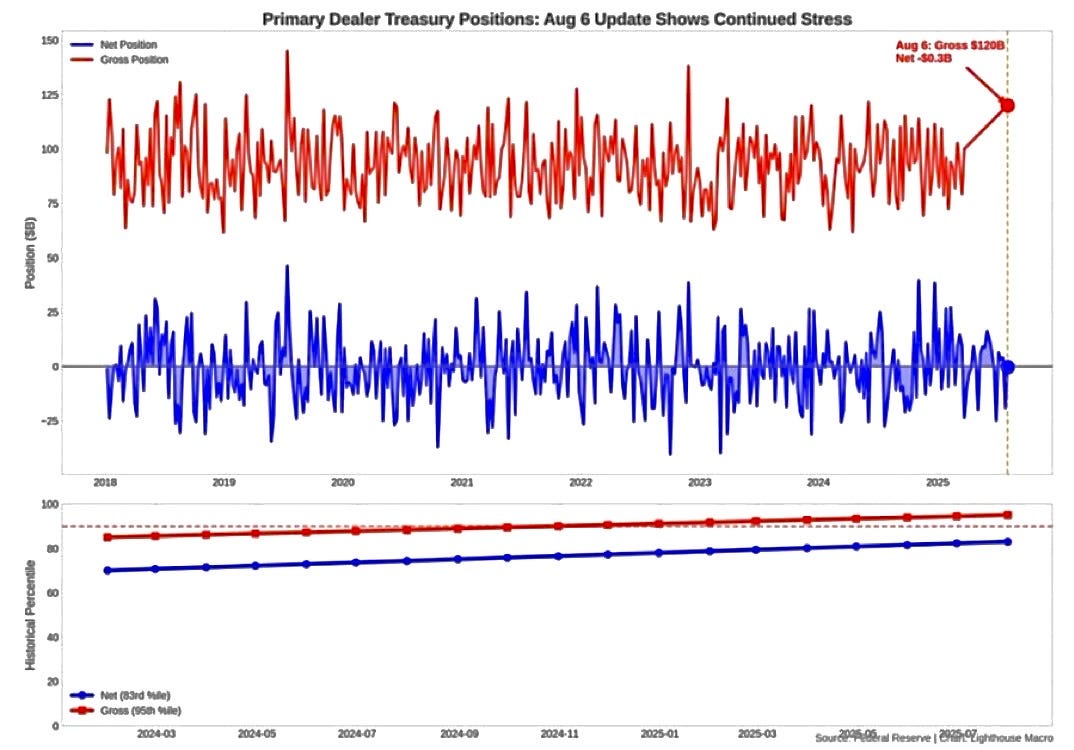

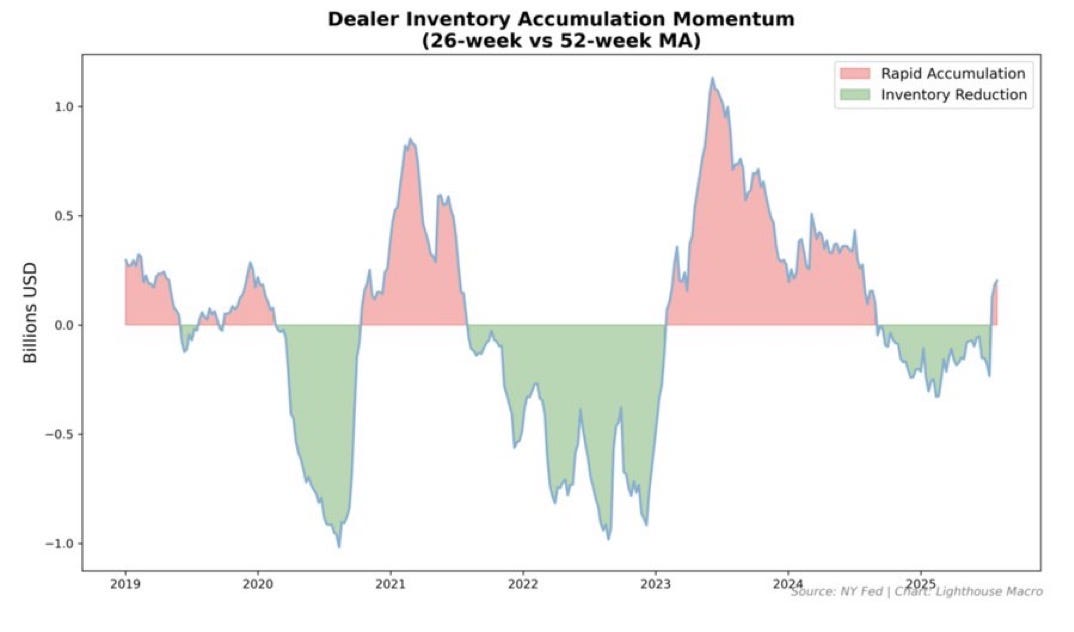

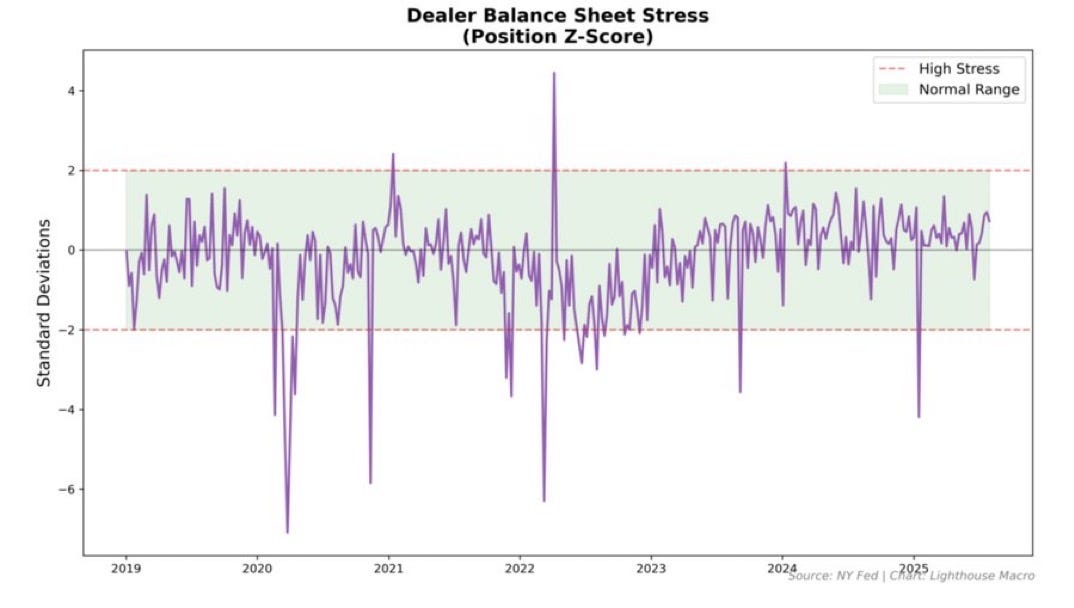

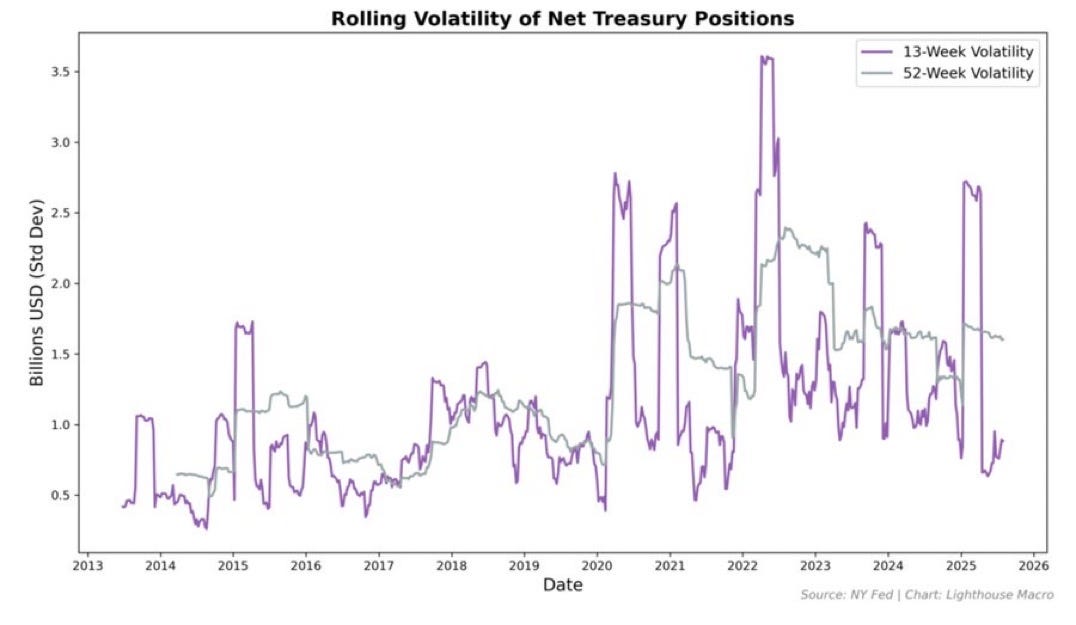

Primary dealer inventory has surged to $120 billion, placing it at the 96th percentile historically. With Supplementary Leverage Ratio (SLR) constraints binding, dealers are operating at 96% of their regulatory ceiling. Our dealer accumulation momentum indicator shows sustained, rapid accumulation throughout 2024-25, with short-term accumulation consistently exceeding long-term trends—a classic sign that dealers are absorbing inventory faster than they can distribute it.

When dealers can't warehouse bonds, auctions fail or yields spike—sometimes both. The stress is already visible: 45% of 2025 auctions have tailed, signaling persistent weakness in long-end demand.

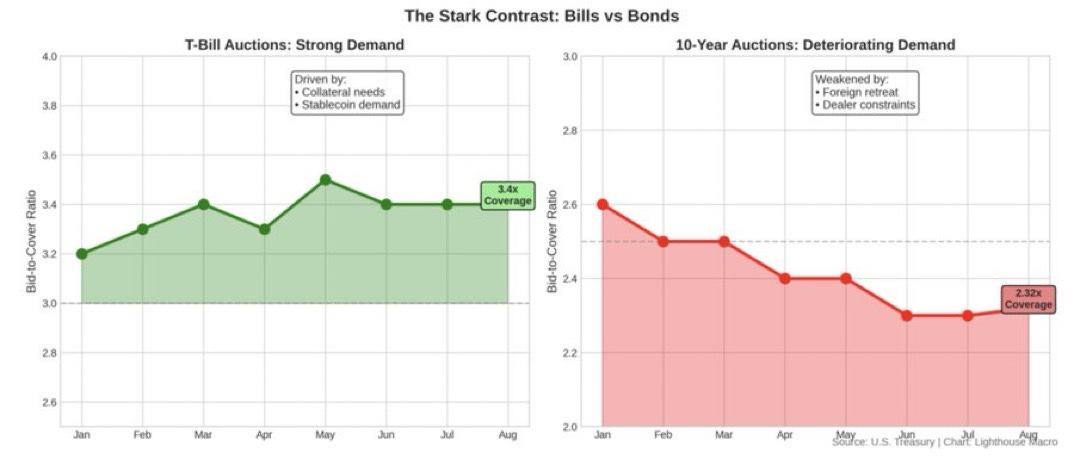

The Bill-Bond Divergence

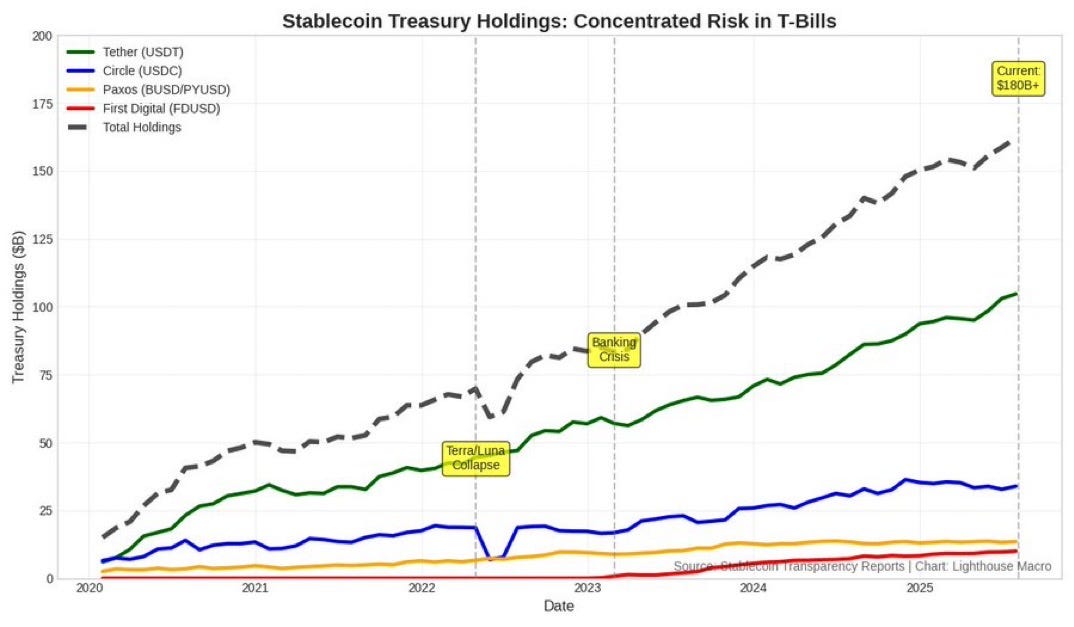

The contrast between the short and long ends of the curve reveals the technical versus fundamental nature of current demand. T-bill auctions remain well-bid with 3.4x coverage ratios, driven by collateral needs and the rise of stablecoin issuers who now hold over $180 billion in T-bills (with Tether alone accounting for $125 billion).

But 10-year note auctions are deteriorating, with bid-to-cover falling to 2.32x. The front end is strong for technical reasons—regulatory requirements and crypto backing needs. The long end is weak for fundamental ones—a genuine lack of natural buyers at current yield levels.

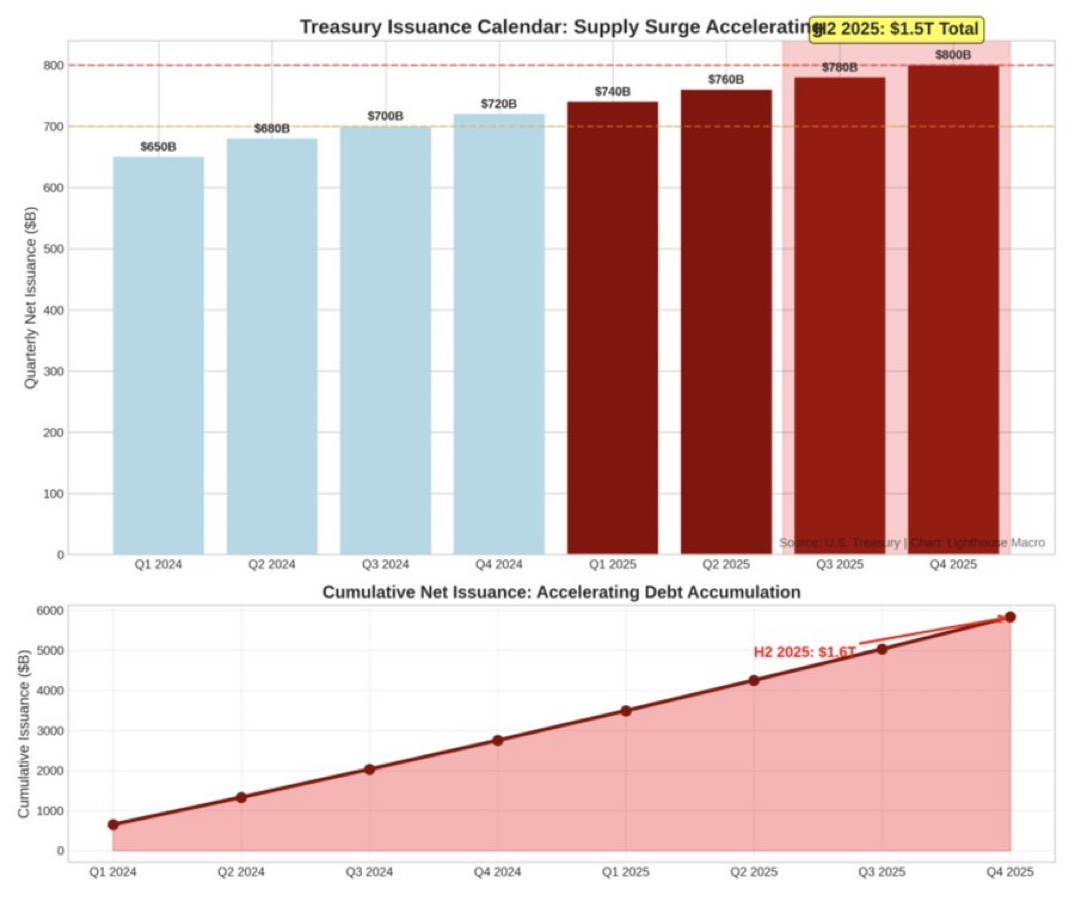

Supply Surge Meets Constrained Demand

The Treasury's issuance calendar compounds these problems. Net issuance will reach $1.5 trillion in H2 2025, with quarterly totals rising from $700 billion to $800 billion. This supply surge comes precisely when traditional buyers are retreating and intermediaries are constrained.

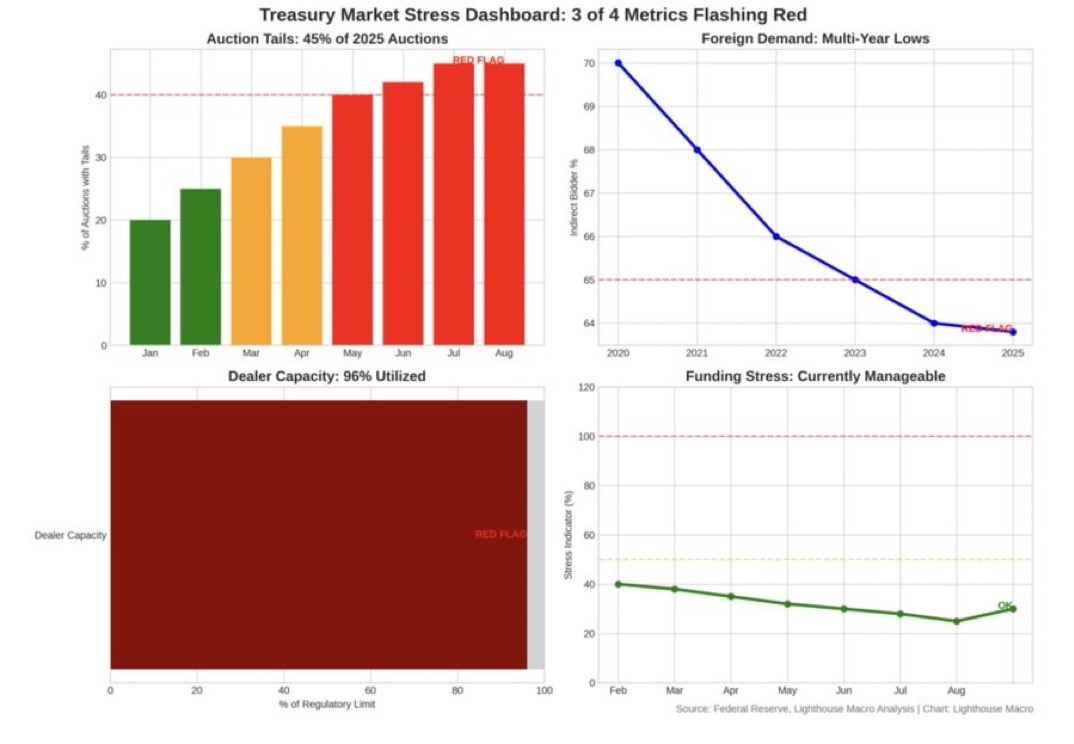

Our stress dashboard shows 3 of 4 metrics flashing red:

* 45% of auctions tailing

* Foreign demand at multi-year lows (63.8%)

* Dealer capacity at 96%

* Only funding stress remains manageable at 30%

The convergence of these warning signals with $1.5 trillion in upcoming issuance suggests the market's ability to absorb supply without significant yield concessions is increasingly questionable.

Stress Scenarios and Market Impact

If foreign demand continues declining and dealers hit capacity constraints, our models suggest 10-year yields could reach 4.75%-5.00%. In a severe scenario with forced selling, yields could spike above 5%. The curve would bear-steepen violently, with long rates rising faster than short rates.

The Fed faces an impossible choice. Cutting rates risks stoking inflation fears that drive long yields higher. Holding steady means watching dealers and banks struggle under the weight of inventory. Either path leads to stress, making continued long-end weakness the highest conviction outcome regardless of Fed policy.

The New Reality

The real risk is that weak auctions become routine and markets stop treating Treasuries as the world's safest asset. Once that perception shifts, there's no easy way back. The August 6 1.125bp tail may be remembered as the canary in the coal mine—the first clear signal that the perpetual bid for U.S. debt is breaking down.

Treasury markets are transitioning from an era of abundant natural demand to one of constrained intermediation. Investors should prepare for:

Structurally higher volatility

Wider bid-ask spreads

Periodic dislocations

Reduced liquidity at tight spreads

The days of assuming infinite liquidity at tight spreads are over. Position accordingly.